NielsenIQ: Inflationary growth of sales value in organized retail

The development of the Greek retail trade for the first half of 2023 is characterized as "inflationary" by NielsenIQ.

Wednesday, August 16, 2023

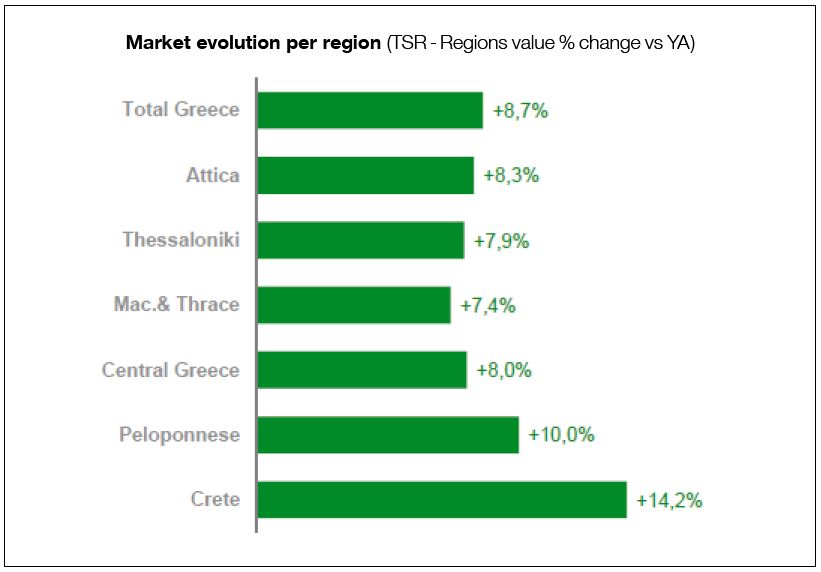

In fact, based on the latest data available to NielsenIQ, in which it is noted that the actual data from the "discount channel" is now included, the Greek organized food retail market, in mainland Greece and Crete, excluding the Greek islands, moved positively in terms of sales value, by 8.7% in the first half of 2023, compared to the first half of 2022.

The trend is mainly driven by food, both fresh, which shows an increase in value by 9.2%, and standardized, which "rises" in sales value by 9.4%. Bazaar products showed the most modest growth, at 2.7%, according to NielsenIQ. At the same time, the major FMCG categories of household fast moving consumer goods (FMCG) and personal care are showing significant sales growth in value, by 10.6% and 7.8% respectively. Looking at sales by volume for all FMCG products - up to Sunday 18th June 2023, it is observed that they show a negative trend, i.e. a decrease of 2.5% which suggests that the growth of the market is purely inflationary, with total consumption to be limited.

Deconstructing the market into the different typologies of stores, in the different geographic areas, as defined by NielsenIQ, interesting findings emerge: Regarding the different types of stores, the largest growth is shown by the stores that are larger in square meters, with the first hypermarkets , i.e. stores over 2,500 m2: They show an increase in sales value of 13.4%, which is possibly due to the increasing tendency of consumers to look for more offers, but also more competitive, therefore lower prices. At the level of geographical regions, tourism seems to have already significantly emphasized the purchasing dynamics of the Greek region: The regions of Crete and the Peloponnese show the most positive developments, by 14.2% and 10% respectively.

The rally of private label products continues upwards

Focusing NielsenIQ’s analysis of available data on price developments, after a record 13.5% increase in prices in the last quarter of 2022, there appears to be a gradual de-escalation from the beginning of 2023 the rate of increase, although it continues to be maintained at double-digit levels: 11.1% from the beginning of April to June 18, 2023. It is also noted that consumers, in their effort to limit the so-called "out of pocket" per purchase “travel”, continue to show a growing preference for private label products. The latter have significantly increased their average selling price, but continue to be the cheapest alternative in the majority of categories, having now reached a market share of 24.8%. If we look at the specific share in the large category of home care products, we find it at 35.2%, almost 2% higher than at the end of 2022.

More and stronger promotional actions instead of constant price list reductions

Retailers and suppliers are stepping up their efforts to be as competitive as possible by offering shoppers more and more deals, rather than the strategy of strategic contractual reductions in list prices. The rate of promotional intensity in the market has reached the impressive rate of 69.3% for the first half of the year, at least as far as branded FMCG products are concerned.

Source: Food Reporter #1005/2023-07-28