Organized Retail: The increased consolidation, the Private Label fightback, and this year’s estimates

What NielsenIQ’s ’2022 Retail Battlefield, Market Overview and Retail Landscape’ survey shows

Tuesday, April 18, 2023

NielsenIQ gave the pulse of 2022 consumer buying behavior and retail prospects for 2023 through a full suite of research presentations at its annual Shopper Trends Event 2023 held on March 30, 2023, at Anassa City Events.

Appreciating the said market in 2022, it will be around 13.5 billion euros, with the ten strongest retail players having a concentration of 82.3%, according to the presentation of the research "2022 Retail Battlefield, Market Overview and Retail Landscape” says Alexandros Floros, Retail Vertical Leader Mediterranean cluster of NielsenIQ.

It is noted that organized retail trade, from 2010 to 2021, is seeing a growth of only 1.3% at store level. "The concentration in organized retail is a result of the investments made in it, but it is also the result of a consolidation and contraction that exists in the traditional" Mr. Floros further explains the reason for the development of organized retail in Greece.

With +6.4%, the fast-moving categories moved in the total turnover

With regard to the evolution of the two channels, i.e. retail stores and cash & carry together, in 2022 they increased with a trend of 7.1% compared to 2021. "In the total turnover, the fast-moving categories moved to +6.4 %, the bazaars had almost a flat development maintaining 5.5%, while the categories of fresh products moved to 8.3%", points out Alexandros Floros. Regarding Cash and Carry, total turnover increased by 14.7%, being a channel that continues to recover from the effects of the pandemic.

Mr. Floros highlights for the fast-moving categories, among other things, that the weighted price change moved to 7.9% in 2022. "If we deflate the turnover we saw last year in the channel, the volume contraction was only at -1.5 %". Regarding food categories, inflation was observed at 8.2% in 2022 and a contraction in consumption at 1.1%.

Private label products trended 17.3% in total sales in 2022

In addition, focusing on private label products, they increased their share and reached 23.8% in total with the purchase of discounters products and 14.8% in the market without them.

Noteworthy is the fact that private label products moved with a trend of 17.3% in their sales throughout the year. "At the beginning of the year, private label products were more restrained in their price changes, while from March 2022 onwards, the rate of their price change gradually begins to be greater than that of branded products" states Alexandros Floros regarding price fluctuations of private label products due to inflation. In addition, it is worth mentioning that 2 out of 3 branded products that were sold were under a promotion (66.7%).

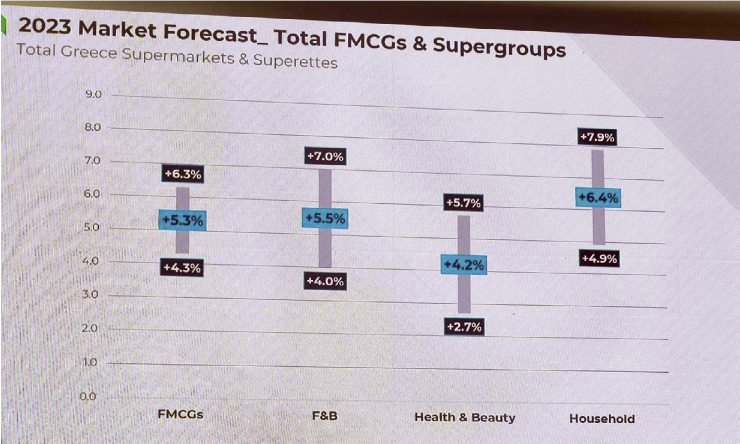

What do we expect in 2023?

The increase in inflation of the organized channel, which has lagged behind compared to the rest of the country’s economy, will contribute to the de-escalation of inflation in the second half of 2023. +5.3% (with plus - minus one unit of deviation) at the level of turnover" says Mr. Floros, who adds that for the individual category of food and beverages, it is expected to reach +5.5%, with a larger deviation (+4% to +7%).

Source: Food Reporter #0925/2023-03-31